Corporate Hedging Could Be Prediction Markets’ Next Major Use Case

Susquehanna’s $500 million World Cup initiative tests whether event contracts can move beyond trading volume and become practical corporate risk-management tools.

Prediction markets have spent much of the World Cup proving that they can attract retail trading volume. This week offered a more consequential development: can the same markets become a tool for hedging financial risk at the institutional level?

Susquehanna International Group said this week it has lined up $500 million to help companies hedge World Cup-linked financial exposure through prediction markets. This is one of the largest institutional commitments yet to the idea that event contracts could function as a corporate risk-management tool.

The capacity is intended for companies whose revenues or liabilities may change depending on the tournament outcomes, including sponsors, broadcasters, hospitality businesses and consumer brands.

What the hedge could look like

Consider a consumer brand offering customers $100 million in rebates if France wins the World Cup. That promotion creates a contingent liability: if France loses, the rebate is never paid; if France wins, the company owes $100 million. The brand could buy France “Yes” contracts that pay out on the same outcome, using the proceeds to offset part of the rebate bill.

The objective is not necessarily to profit from predicting France correctly, but to exchange an uncertain and potentially large expense for a smaller, more predictable hedging cost. The same logic applies to broadcasters exposed to audience swings, retailers holding team-specific inventory, sponsors with performance-linked commitments and travel businesses whose demand changes as teams advance or exit.

While this is a welcome development for the prediction-market sector, the hedge can only be as effective as the contract’s fit with the underlying exposure. A World Cup winner market may not fully protect a broadcaster whose revenues rise round by round, or a hotel group whose losses depend on where fans travel rather than which team ultimately lifts the trophy.

Companies may therefore need several contracts covering qualification, progression and the final outcome, creating basis risk if the market payout and the commercial loss do not move together.

Liquidity is another constraint; A recent CNBC analysis of Polymarket found that roughly 70% of closed markets recorded less than $10,000 in total trading volume, while more than 45,000 markets closed without a single trade. Fewer than one in ten exceeded $100,000.

This leaves the corporate hedging case concentrated in a much smaller group of contracts, particularly major sports markets where order books appear deeper and the underlying commercial exposure is easier to identify.

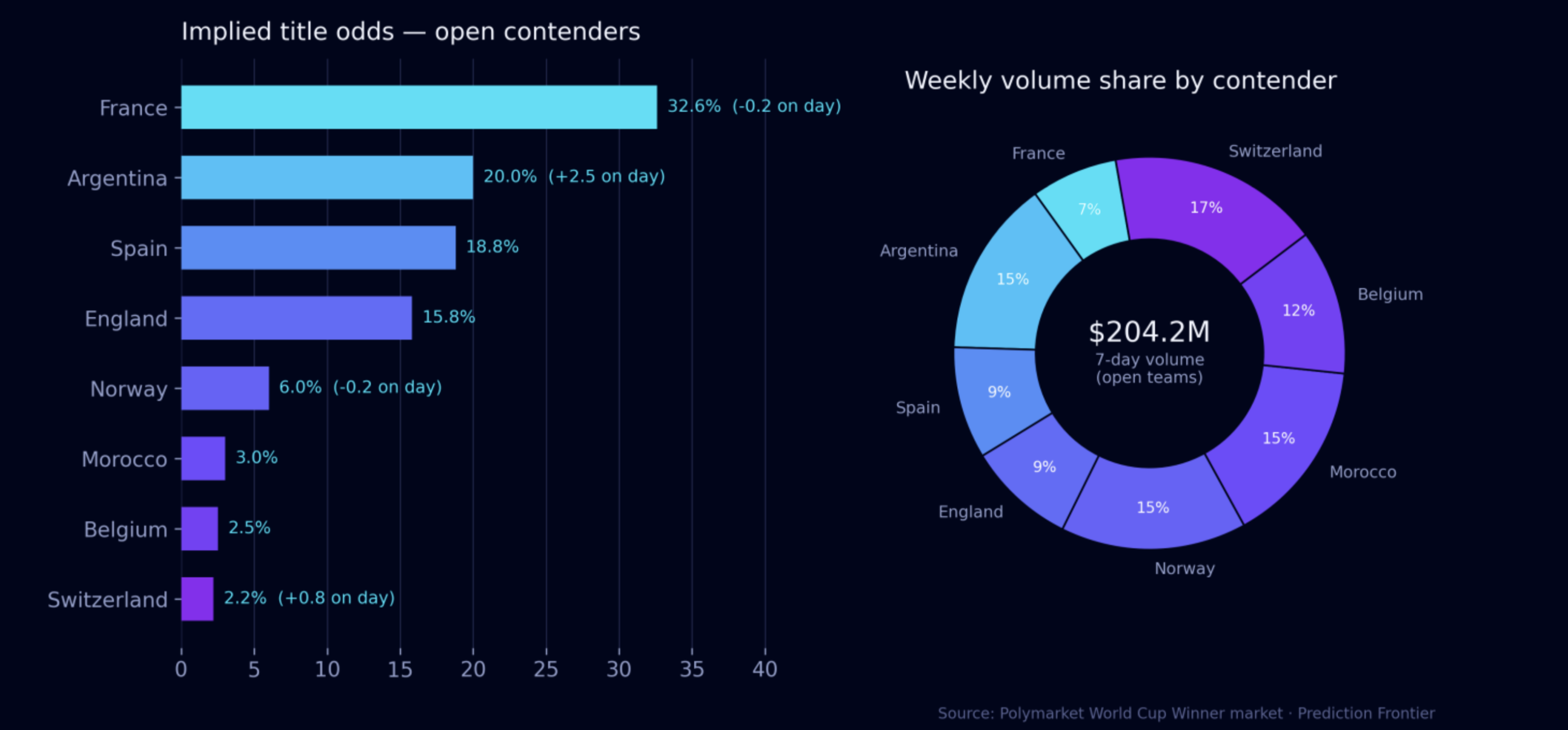

World Cup Numbers in a Prediction Markets Lens

The chart captures the market before the quarter-finals, when title probability had consolidated around France, Argentina, Spain and England. France led at 32.6%, while those four teams together accounted for roughly 87% of the board.

The weekly volume distribution told a different story: Switzerland, Norway and Morocco drew some of the heaviest trading despite carrying much lower title probabilities, a familiar knockout-stage pattern in which traders chase the larger payouts attached to outsiders rather than continue buying an already expensive favourite.

France has since beaten Morocco 2–0 and become the first team through to the semi-finals. Its title price has moved to roughly 39%, ahead of Argentina at 18% and Spain at 17%, according to Polymarket’s latest market view.

Les Bleus now wait for the winner of Spain–Belgium, while England–Norway and Argentina–Switzerland complete the remaining quarter-finals. The move from 32.6% to around 39% is meaningful, but not dramatic: the market had already priced France as a strong favourite against Morocco, so much of the expected result was embedded before kick-off.

The larger repricing should come from the remaining ties, where the elimination of Spain, Argentina or England would remove one of the few teams still carrying a material share of the title probability.

The elimination chart remains the sharper illustration of how these markets behave under pressure. Brazil lost 6.4 percentage points of title probability on the day it went out; Portugal shed 5.8, while the Netherlands and Germany fell to zero within the week. Across a winner market that has generated about $4 billion in lifetime volume, large amounts of implied probability continue to disappear within hours of the final whistle.

Market Manipulation Hits Again

Spotify challenged Kalshi and Polymarket this week, demanding both platforms remove its logos and state clearly that no partnership exists, after the company caught more than 500,000 artificially generated streams that briefly pushed a Malcolm Todd track into contention on a Kalshi contract for the most-streamed US song in June — a market that had traded roughly $3 million in volume. A trader who says he flagged the anomaly early put his own losses at $4,500 and accused Kalshi of moving too slowly; Kalshi says it's investigating with Spotify.

Stuart Crowley, Commercial Director at NEXTPredict, made an intriguing commentary on this case: prediction markets get talked about as liquidity businesses, but rights, data, and permission may end up being some of the more interesting moats. Sport is where the pattern is showing up first — Bundesliga, NHL, MLB, UFC — because the questions are unavoidable once real money and a league's reputation are riding on the outcome: can a rights holder control how its brand shows up on a betting-adjacent product, and can it trust the settlement data?

The read is that the same questions eventually reach the Oscars, Grammys, reality TV, and streaming charts — anywhere fandom gathers around outcomes, there is IP, data, brand permission and reputational risk sitting underneath the fun.

Regulators Outside the US Begin Defining the Category

While most industry attention remains fixed on the US, regulators elsewhere are beginning to define prediction markets through their own existing frameworks.

ESMA issued a statement warning that some event contracts may qualify as financial instruments under MiFID II and fall within national restrictions on binary options. The regulator’s position is that classification depends on the contract’s underlying event and economic structure, not whether the operator calls it an event contract or prediction market.

Not every event contract will receive the same treatment. Some may instead fall under national gambling law or, depending on their design, the EU’s crypto-asset framework. But operators cannot assume that the category exists outside existing financial regulation simply because the technology or terminology is new.

South Korea is taking a different route. Its media review authority has agreed to hear Polymarket’s position before determining whether corrective action is warranted over possible gambling-law violations. No final illegality finding or blocking order has yet been issued.

Together, the two developments point to a more fragmented international market. The same event contract may be treated as a derivative, binary option, gambling product or crypto-linked service depending on where it is offered.

The World Cup has shown that prediction markets can scale globally. The next stage will test whether their liquidity, settlement sources, commercial rights and regulatory structures can scale with them.

Stay ahead of the prediction markets industry. Subscribe to Prediction Frontier for weekly intelligence on market structure, regulation, institutional adoption, data and emerging use cases.