Prediction Markets Hit Record Volumes as Institutional Interest and Scrutiny Intensify

World Cup trading is driving unprecedented activity, while Cboe, Tradeweb and Meta bring new institutional and consumer attention to a sector facing sharper legal and conduct questions.

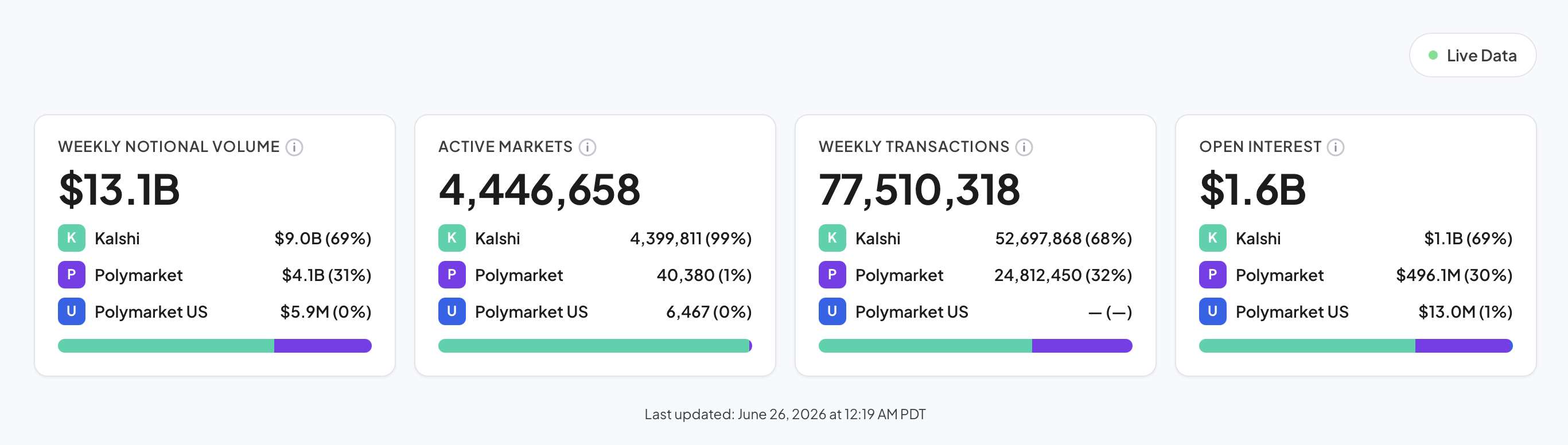

Prediction Markets have continued to break records in trading volume since the debut of the FIFA World Cup 2026. According to DeFi Rate, the past week recorded a total notional volume of $13.1 billion; Kalshi accounted for $9B (69%) while Polymarket contributed $4.1 billion.

Total weekly transactions stand at 77.5 million, and the Open Interest across Kalshi and Polymarket’s event contracts is currently at $1.6 billion.

One interesting observation is that sports account for most of the activity; Kalshi’s 7-day sports volume is at $2.9 billion, crypto follows at a distance with $652 million. Polymarket’s stats also tell a similar story, with the weekly volume at $1.9 billion and crypto at $278 million.

The next few weeks will likely be more momentous as the World Cup group stages come to a close. For the first time in history, we have a World Cup that’s also a financial market; a concept that has resonated beyond the traditional sports fan base to traders, institutions, and crypto users, among a broader global audience.

Institutions and Distribution Are Starting to Form

The prediction market sector is also beginning to attract interest beyond its existing retail and crypto-native user base.

This week, Cboe launched Cboe Predicts, a suite of binary options linked to the Mini-S&P 500 Index. Its first contracts, XSPBW and XSPBX, are already available through Interactive Brokers and are expected to reach Charles Schwab clients in the coming months.

It is worth noting that the product is structurally different from the event contracts currently driving prediction market volume. Cboe’s contracts are securities-based listed options, centrally cleared through the Options Clearing Corporation, and pay $100 or zero depending on where the Mini-S&P 500 settles relative to a specified level. Rather than operating through the CFTC’s event-contract framework, Cboe is bringing outcome-based trading into established options-market infrastructure.

Meanwhile, Tradeweb made a parallel move on the institutional-data side. The electronic trading platform launched a dedicated Kalshi pricing page for U.S. institutional clients this week, allowing them to monitor real-time market-implied probabilities across political, economic, financial and global events alongside its existing analytics and execution tools. Kalshi’s American Power Index, a composite measure of market-implied U.S. political and policy risk, is expected to follow in July.

The most notable development came from a New York Times article, which reported that Mark Zuckerberg has directed a small team to develop a standalone prediction product internally called Arena. The app would initially use a points-based system rather than real money, though Meta has not ruled out financial transactions in later versions.

These moves are evidence of a niche sector whose institutional and distribution layers are forming across several touchpoints. Cboe is adapting outcome-based products to established options infrastructure; Tradeweb is incorporating event-market data into institutional workflows; and Meta is testing whether prediction products can scale through mass-market consumer distribution.

Kalshi Seeks $40 Billion Valuation in Fresh Funding Talks

Kalshi is reportedly in talks to raise new capital at a valuation of about $40 billion, according to the Financial Times. The discussions come only weeks after the company closed a $1 billion Series F at a $22 billion valuation. If the new round closes at the reported figure, Kalshi's valuation will have nearly doubled in roughly seven weeks.

To appreciate the pace: Kalshi was valued at $2 billion in June 2025, $5 billion by October, $11 billion by December, $22 billion in May 2026, and is now in discussions at $40 billion.

The Information also reported that Kalshi had surpassed $2 billion in annualised revenue. At a reported $40 billion fundraising target, that would imply a valuation-to-annualised-revenue multiple of roughly 20 times. Whether investors ultimately assess the company more like exchange infrastructure, a brokerage platform or consumer fintech remains an open question.

Kalshi CEO Tarek Mansour said in a CNBC interview on Wednesday that the company intends to pursue an eventual IPO, but that it will not list in 2026. Separately, the Financial Times reported that Kalshi’s proposed funding round could close as early as the third quarter of 2026.

One number is worth holding alongside the reported valuation. The Financial Times estimated earlier this year that sports contracts accounted for roughly 90% of Kalshi’s annualised revenue, making the category central to the company’s current growth story.

That same category remains at the centre of the state-level legal disputes. In its June 17 lawsuit, Kentucky alleged that approximately 89% of Kalshi’s 2025 contract volume was tied to sports, out of nearly $23 billion in total contract volume for the year. Kalshi disputes the premise of these actions, maintaining that its contracts fall under federal commodities regulation rather than state gaming law.

The legal question remains commercially material: whether courts accept the federal pre-emption argument, or allow states to apply their own sports-wagering rules to these contracts. That outcome could materially affect the durability of the growth and valuation assumptions now being attached to the business.

Polymarket's Promotional Campaign Draws Scrutiny

The Wall Street Journal published an investigation on June 21, finding that Polymarket paid a network of mostly college-age content creators between $2,000 and $3,000 per month to post videos depicting winning bets in a campaign that reached over 140 million views.

According to the Journal's review of more than 1,100 videos spanning December 2025 to mid-May 2026, the trades were filmed on dummy websites built to resemble the live platform rather than on Polymarket itself. Creators depicted roughly $1.9 million in winnings across 118 videos; the Journal found the same bets on the actual platform would have resulted in losses.

The CFTC and FTC both declined to comment on whether they plan to examine the findings. Polymarket said it is auditing its promotional content and is committed to accurate and transparent markets, without directly addressing the Journal's specific findings.

This is the second disclosure-related report in a month. In early June, Politico reported that Polymarket's marketing director used a personal PayPal account to pay creators for promotional content without disclosure. The Journal also found that paid creators promoted at least 19 videos discussing the use of non-public information to trade, a practice Polymarket's own rules prohibit.

For a sector still making its case to regulators and institutional investors, how platforms handle marketing and disclosure will likely become as scrutinised as how they handle market resolution. Polymarket has said it will conduct a full audit; the results of that review will matter.