Solving the Jump Problem: Can We Finally Bring Leverage to Prediction Markets?

We’re looking at the most credible solutions on the table, who’s building them, and what trade-offs come with each.

This is Part III of the Prediction Markets Intelligence Series. If you’re new here, here’s the arc:

Part I — “How Prediction Markets Work and Why They’re Smarter Than Any Single Expert” — shows why crowds consistently beat experts, and how prediction markets aggregate dispersed private information into prices that outperform even the most seasoned analysts. (Read it if you want to understand why this whole space matters.)

Part II — “The Jump Problem” — established the core structural barrier: prediction market prices don’t drift; they snap. This makes traditional leverage mechanics — margin calls, continuous liquidation — fundamentally unworkable. (Read it before this one if you haven’t. It will break your assumptions about leverage in a useful way.)

Part III — this piece — is the payoff. We’re looking at the most credible solutions on the table, who’s building them, and what trade-offs come with each.

Laying down the foundation

Imagine you’re 90% sure the Fed won’t cut rates today.

You’ve done your homework. You’ve read the minutes, tracked the language shifts, and priced the probability yourself. You want to bet big. You want to put real size behind your conviction.

But no platform will let you leverage your position.

Why? Because in a prediction market, the moment that the announcement drops, your position doesn’t slide. It teleports. From $0.90 to $0. Instantly. There’s no gradual decline, no time to call the broker, no grace period. The bet simply ends — and if you’d borrowed money to make it bigger, every penny of that borrowed capital is gone before you can blink.

This is the jump problem. It’s why the biggest prediction market platforms refuse to offer leverage. And it’s why brilliant people across crypto, DeFi, and traditional finance are working furiously to crack it.

So, what if there’s a way to work with the jump instead of against it?

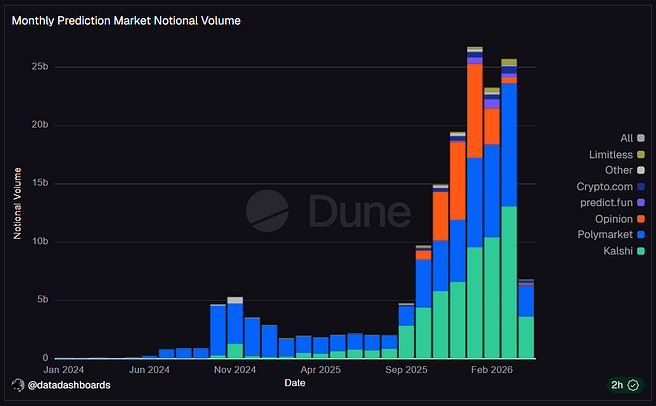

Fig. 1 — Prediction market monthly volume growth, Jan 2024 — Apr 2026. Source: Dune

Why the Jump Problem Is Uniquely Hard

Quick restatement for newcomers, because it matters:

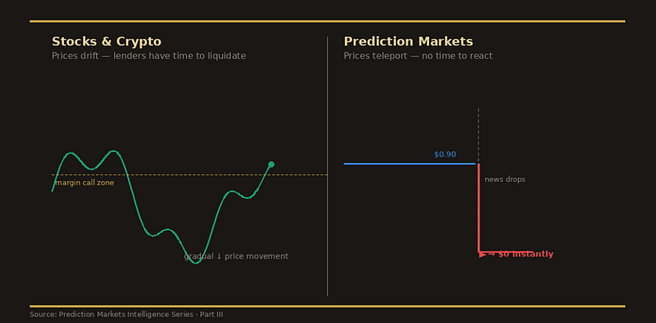

In stocks and crypto, prices move continuously. If a stock drops 10%, a lender can issue a margin call, force a partial liquidation, and recover most of their capital. The move gives them time. In a prediction market, there is no time. A “Trump announces US x Iran ceasefire by May 30” NO contract sitting at 92¢ looks safe — until one tweet drops. The price jumps to $0 in a single moment, with no liquidation window, no warning, no recourse for the lender.

This creates a brutal combination for anyone trying to offer leverage: a bounded payoff ceiling (maximum win is $1), no carry income, no natural hedge, and the ever-present risk of an instantaneous total loss. It’s the worst possible object to leverage.

Fig. 2 — Continuous price movement (stocks/crypto) vs. binary jump (prediction markets). The liquidation engine has no time to run.

Now consider the scale at stake. According to Benny Attar’s Setira Research, prediction markets have grown to nearly $10 billion in weekly trading volume. That sounds impressive until you compare it to US equity markets — which trade roughly $400–500 billion per day. Leverage is one of the primary mechanisms by which asset classes scale. Until prediction markets solve the jump problem, that ceiling stays firmly in place.

“Prediction markets are not just another trading venue. They are a new asset class with their own microstructure — and their own pricing rules.”

Cracking The Jump Problem

Over the past few months, I have looked into the jump problem, reading extensively about what solutions are available and whether they are worth the trouble. Here are some of the solutions I found:

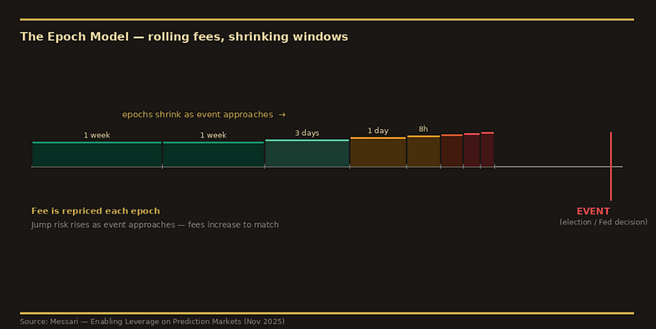

Solution 1: The Epoch Model — Rolling Fees Instead of Upfront Bets

“The epoch model does for prediction market leverage what funding rates did for crypto perpetuals.”

The central insight from Messari analyst Kaleb Rasmussen: the reason it’s nearly impossible to price leverage upfront is that you’d need to forecast jump risk, drift, and volatility across months. That’s not tractable. Instead, break the position’s life into short, defined windows called epochs.

Each epoch, the trader pays a rolling fee to the financier — similar to how funding rates work in perpetual futures. The epoch can be fixed or adaptive: for an election market, start with weekly epochs months out, then shrink to hours as election day approaches. For a Fed decision, time the epochs around the specific announcement window.

Fig. 3 — The Epoch Model: epochs shrink as the event approaches, allowing the financier to reprice jump risk at each rollover. Source: Messari (Nov 2025).

The fee formula (without the math): Fee = Leverage × (Jump Risk + Creep Risk) + Funding Cost. Jump risk does most of the damage. Creep risk — gradual price drift that a liquidation engine can handle — is smaller but still real.

This converts an impossible long-term pricing problem into a tractable short-term one. “What’s the probability this market jumps to zero in the next 8 hours?” is answerable. “What’s the probability over the next six months?” is not.

Think of it like car insurance, month-to-month instead of one lump sum for your whole life. You reprice risk as conditions change.

Critical caveat: If resolution is effectively instantaneous and jumps are perfectly priced, the fee wipes out any benefit from leverage. This only works when there’s time to liquidate before full resolution — which makes faster platform infrastructure a prerequisite, not an afterthought.

Solution 2: Auction-Based Jump Capture

Another architectural idea from the Messari paper: build a prediction market platform that holds a short auction the moment a major news event hits — before the resolution finalises.

The logic: when news breaks, arbitrageurs immediately try to profit from the price jump. An auction mechanism could capture some of that arbitrage profit and rebate it back to the financiers and market makers who were caught on the wrong side. Think of it as a “jump tax” on arbitrageurs that funds a “jump insurance” pool for lenders.

It’s directionally promising. Technically, it’s hard — designing a real-time auction that captures value without introducing manipulation risk is a serious engineering challenge. But it’s the kind of idea that rewards the platform willing to invest in infrastructure.

Solution 3: Faster Reaction Windows

Separate from the epoch model’s fee structure, Messari identifies a complementary lever: financiers who react faster lose less. The faster a platform can detect a price move and execute a liquidation, the less “creep loss” they absorb before the position closes.

This means investing in faster infrastructure and smarter alert systems. It also means caps: higher margin requirements and reduced leverage ratios during high-risk windows — the 24 hours before a Fed decision, or election day itself. This doesn’t solve jump risk. But it meaningfully reduces the damage from creep, which makes the overall fee lower and the product more viable for traders.

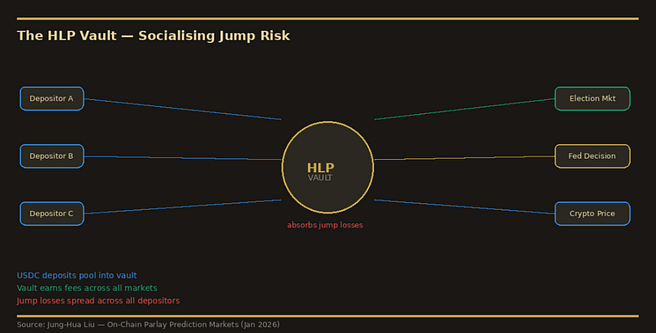

Solution 4: The HLP Vault Model — Socialising Jump Risk

Source: Jung-Hua Liu — “On-Chain Parlay Prediction Markets with Deep Liquidity” (January 2026)

Fig. 4 — The HLP Vault Model: jump risk is socialised across depositors, who earn fees across all markets in return. Source: Jung-Hua Liu (Jan 2026).

Instead of individual financiers absorbing jump risk alone, pool capital into a community-owned liquidity vault. Analogous to Hyperliquid’s HLP model, a Hybrid Liquidity Provider vault accepts USDC deposits from multiple participants, acts as the market maker, and backstops leveraged positions across thousands of markets simultaneously.

When a jump event hits, the loss is spread across all depositors. And because the vault earns fees and liquidation penalties across those same thousands of markets, losses in one are offset by gains in others. The vault becomes the house — and like any house, it wins over time if the pricing is right.

The caveat: Vault depositors become the counterparty of last resort. If multiple high-profile markets jump simultaneously — as they might during a major political shock — the correlated losses can overwhelm the diversification benefit. Depositors need to understand they are not passive yield earners. They are underwriters.

Solution 5: Parlay-Style Synthetic Leverage

The most creative workaround on this list. Instead of borrowing money to amplify a single prediction, combine multiple bets into a parlay — where every leg must win for the payout to trigger. The multi-leg structure creates a leveraged-like payoff profile without any borrowing, any lender, any liquidation engine, and crucially, any jump problem for the platform.

The risk is fully pre-collateralised and sits entirely with the bettor. There’s no counterparty exposure. Multi-leg parlays already account for over 70% of revenue in traditional sportsbooks, and several on-chain prediction market architectures are now building this capability specifically for event contracts.

The honest framing: this is not true leverage. It doesn’t improve capital efficiency or let you express a larger position with less capital. It multiplies risk across events rather than amplifying a single bet. But for many retail participants, the feel of leverage is what they want — and parlays deliver that without the structural nightmare of lender exposure to binary jumps.

The Honest Trade-offs

Every solution on this list has a cost. Worth naming them directly:

The epoch model reduces the pricing problem but may produce fees so high that smaller traders are effectively priced out of leveraged positions.

Auction mechanisms add complexity and introduce new attack surfaces — anyone who knows when news is about to drop can game the auction.

HLP vaults shift risk to depositors who may collectively underestimate what it means to be short-correlated jump events across multiple markets simultaneously.

Synthetic leverage via parlays isn’t leverage. It’s risk multiplication without capital efficiency. It solves a perception problem, not the underlying structural one.

No solution is perfect. The question is which trade-offs the market can live with — and which trade-offs regulators, liquidity providers, and retail participants will eventually force to the surface.

The jump problem may not be fully solved yet. And that’s precisely the point. We’re in the room where the work is happening — and the room is open.

“When the jump hits, there’s no time to liquidate. The price teleports. The question isn’t whether this is hard — it’s whether the market can build something hard enough to contain it.”

Your Opinion?

The best ideas in this space don’t come from any single researcher or platform. They come from the collision of perspectives — the trader who’s been burned, the engineer who sees the edge case, the economist who draws the formal proof. This series is a vehicle for that collision.

Three questions for you:

Do you think the epoch model makes prediction market leverage genuinely viable, or does it just paper over the fundamental problem?

Is there a sixth solution not on this list? Drop it in the comments. The strongest ideas will make it into future pieces.

Is prediction market leverage something the market should even want — or is the friction protecting something valuable about how these markets work today?

Part IV of this series takes on the question that follows naturally from this one: who actually wins if leverage comes to prediction markets? The informed trader? The protocol? The financier? Or the platforms that build the infrastructure nobody else was willing to build? We’ll go deep on the political economy of the jump solution.