The World Cup Liquidity Test Begins: Can Prediction Markets Keep the Capital?

The World Cup proved prediction markets can attract billions. Now comes the harder test: whether that capital stays as liquidity thins, entertainment trading rises, and regulatory frameworks begin to take shape.

Prediction markets have spent much of the World Cup breaking trading-volume records. This week offered the first indication of what happens when the tournament begins to wind down.

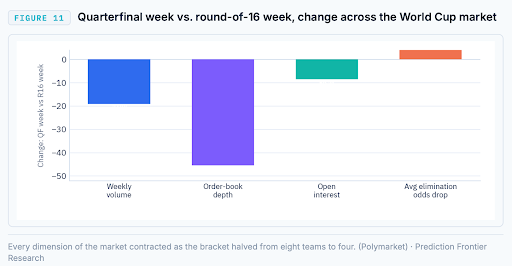

Polymarket’s World Cup Winner market generated $165.6 million in seven-day volume during the quarterfinal week, down 19.1% from $204.6 million the previous week. More significantly, order-book depth fell 45.5% to $29.4 million, while open interest declined by a comparatively modest 8.5% to $61.5 million.

The broader market remains significant. DeFi Rate recorded $13.4 billion in notional volume during the last complete calendar week, with Kalshi accounting for $9.9 billion and Polymarket $3.5 billion. However, the current rolling data reaffirms the reducing activity as the World Cup winds up, with Kalshi’s seven-day volume down 12.6% and Polymarket’s down 35.4% as the final approaches.

The immediate question is therefore no longer whether the World Cup was successful for prediction markets. The tournament has already demonstrated that the platforms can attract a mass audience and process billions of dollars in weekly activity.

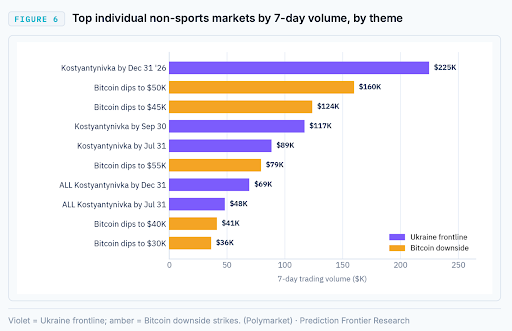

The question is whether that capital can be retained or it will struggle to find its way into other types of event contracts. Politics and crypto markets seem to be likely contenders; isolated non-sports data from Prediction Frontier’s weekly data brief revealed that two markets in particular accounted for the top 10; Will Russia capture Kostyantynivka by...? and Bitcoin’s downside markets.

Entertainment is Taking Over the Truth Engine

DWF Ventures offered another perspective on the type of capital that entered prediction markets during the recent expansion.

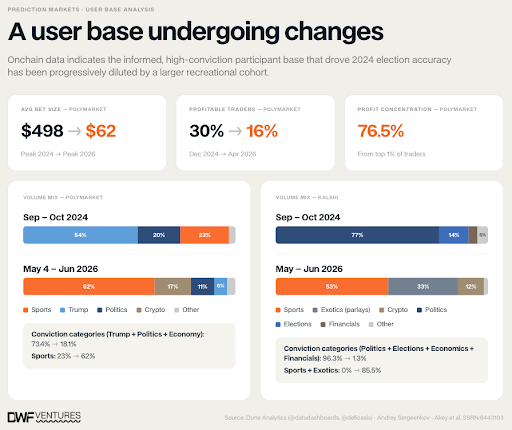

The analysis argues that the composition of the user base has changed considerably since the 2024 US election. Politics, elections and economics accounted for approximately 73% of Polymarket volume and 96% of Kalshi activity during that period. Those categories have since fallen below 20% on Polymarket and 5% on Kalshi, while sports and multi-leg products have taken their place.

DWF also found that Polymarket’s average bet size has declined by more than 85% from its 2024 peak. Meanwhile, exotic contracts, including parlays and combinations, reportedly account for approximately 33% of Kalshi’s volume.

The industry has not simply attracted more capital. It has attracted a different type of capital: smaller positions, higher-frequency participation and users who may be more motivated by entertainment and large potential payouts than by correcting mispriced probabilities.

While recreational activity can increase market-maker revenue, support more contract listings and contribute to tighter spreads when the flow remains inside an order book, entertainment volume does not automatically produce informationally useful liquidity.

The original prediction-market argument was that financially motivated participants with different information and analytical abilities would trade prices toward accurate probabilities.

DWF Ventures puts forward an argument that when a growing portion of activity is driven by team preference, payout size or the appeal of combining several low-probability outcomes, the relationship between volume and forecasting quality becomes less direct.

Gibraltar Writes the First Rulebook

Gibraltar published a standalone prediction-markets regulatory framework this week under its new Gambling Act 2025, the first licensing region anywhere to treat prediction markets as a distinct statutory category rather than folding them into existing betting or financial rules.

Minister Nigel Feetham said the move reflects an acknowledgment that the sector lacks "settled consensus" globally on how it should be classified, and described a framework built on an activity- and risk-based approach covering market manipulation, anti-money-laundering controls, participant protection and operational resilience.

The framework lands as a sharp contrast to the rest of Europe. Nine regulators, including Belgium, France, Germany, Italy, the Netherlands, Poland, Portugal and Spain coordinated a crackdown on unlicensed prediction markets in June, and ESMA has reaffirmed its jurisdiction over binary-outcome, fixed-payout contracts under MiFID II.

Gibraltar is positioning itself as the establishment counterweight: whether the framework becomes a template other jurisdictions adopt is now a live question, particularly for operators currently boxed out of the EU's larger markets and looking for a credible regulatory base to operate from instead.

Insider Trading Reaches the West Wing

The prediction-markets insider-trading story that has dogged the sector all year finally reached the White House itself. Gabriel Perez, Trump's teleprompter operator since 2016, is reportedly in settlement talks with the CFTC over allegations he used advance access to the president's prepared remarks to trade Kalshi's "Mentions" markets, which pay out on whether specific words or phrases are said during a speech.

Sources put his profits above $90,000–$100,000 across more than a dozen speeches, including the February State of the Union and a January address at Davos. Kalshi's surveillance team flagged the pattern, froze most of the associated funds, and referred the case to the CFTC itself.

This case illustrates an unresolved distinction between informed trading and insider trading in prediction markets.

Political analysts forecasting whether a candidate will win an election are aggregating public information and expressing a probabilistic view. A person who has already seen the contents of a speech is not forecasting whether a word will be mentioned since they may possess direct knowledge of the outcome.

In that situation, financial incentives do not improve the market’s information-discovery process; instead, they create a mechanism for monetising privileged access.

Mention markets, corporate-announcement contracts, appointments and certain geopolitical events may therefore require stronger controls than ordinary sports or election markets. These could include restricted-person policies that are already being implemented, contract-specific surveillance, or prohibitions on individuals directly involved in determining the outcome.