What a 46% Liquidity Drop Reveals About How Prediction Markets Actually Work

Inside one World Cup week of prediction market data: a 46% liquidity crunch, a $2B distribution play, and what $1.85B in VC funding says about where this is headed.

TL;DR: A World Cup week where order-book depth fell twice as fast as open interest — and a $2B distribution play that beat every "better product" in the room — reveal how prediction market liquidity and market share actually move.

Something strange happened in the World Cup Winner market this week. Trading volume dipped, which surprised nobody — the quarterfinals produced only four matches against the round of 16's eight, and every pre-tournament favorite survived through to the semifinals. What should raise eyebrows is what happened underneath that volume number. Order-book depth — the actual capital sitting behind quoted prices — fell 46% in seven days. Open interest, the money still committed to unsettled positions, fell by only 8.5%.

That gap — a market losing liquidity more than five times faster than it's losing conviction — isn't really a World Cup story. It's a preview of how this entire industry behaves once real capital gets involved, and one tournament week just made the pattern impossible to miss.

The money that stays, and the money that doesn't

Polymarket's World Cup Winner market turned over $165.6M in the seven days to July 13 — down 19% from the prior week's $204.6M. On its own, that's an unremarkable dip: fewer matches, fewer surprises, less reason to trade. Depth told a sharper story. Four contender books closed as their teams were eliminated, Switzerland's $12.5M chief among them, and market makers pulled quotes rather than reprice into a thinning field. Order-book depth collapsed 46% to $29.4M. Open interest fell only 8.5%, to $61.5M.

The difference matters because the two numbers measure different things. Open interest is a scoreboard of who's still positioned. Depth is a measure of who's still willing to trade around that position. When depth falls twice as fast as open interest, the people with genuine conviction are holding — and the flow that was there for entertainment, not conviction, has already left.

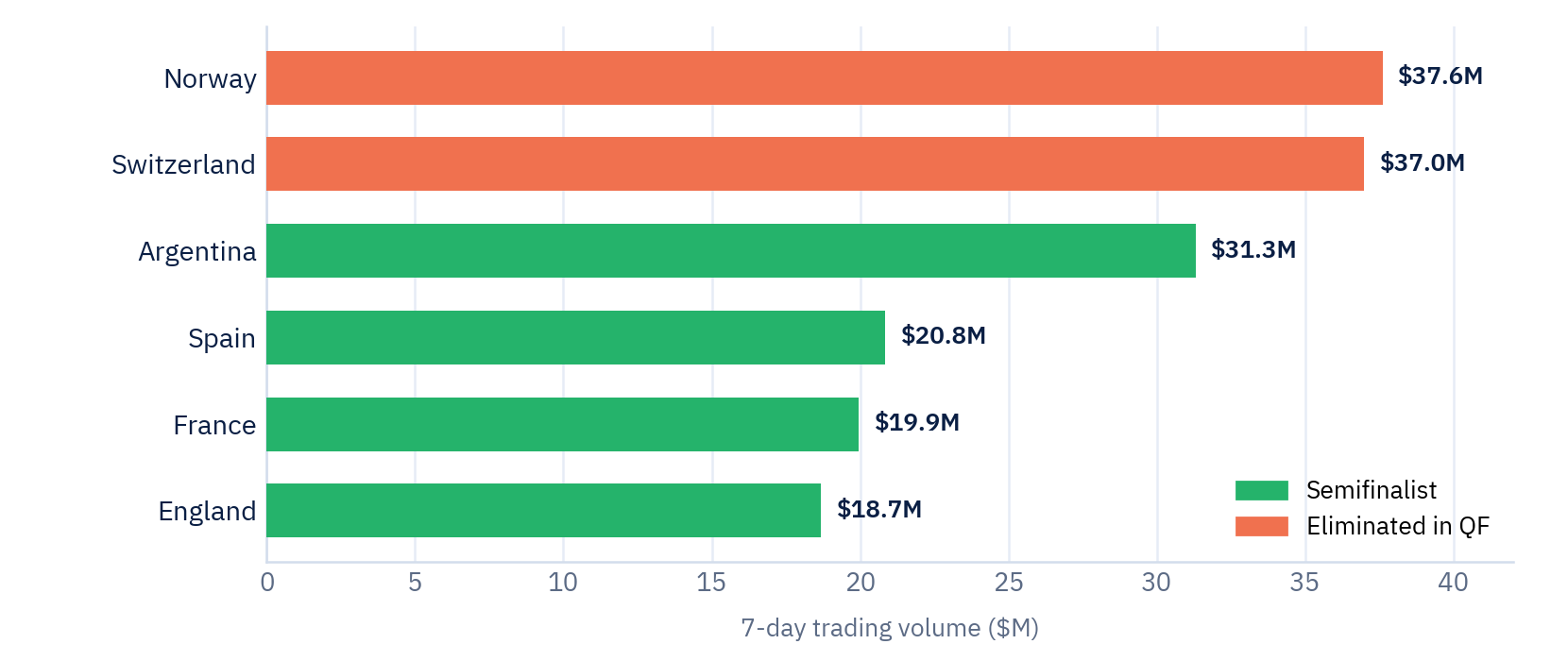

The eliminated-team data makes the split explicit. Norway and Switzerland, both knocked out in the quarterfinals, traded $37.6M and $37.0M respectively over the week — more, combined, than all four surviving semifinalists put together. That's not misplaced optimism. Longshot markets attract lottery-ticket flow right up until the moment they're mathematically dead, and that flow evaporates the instant elimination is final. What's left behind — in France's $6.7M book and the other three survivors — is capital that was never chasing a longshot payout to begin with.

A single week of World Cup data just demonstrated, in miniature, something every liquidity provider in this space already knows and every new entrant has to learn the hard way: retail flow and informed capital are not the same population, and they don't leave a market at the same rate.

It's not a football problem

None of this is unique to a tournament. Zoom out from the World Cup, and the same dynamic — flow concentrating around wherever information is actually resolving — shows up in how the whole market is structured.

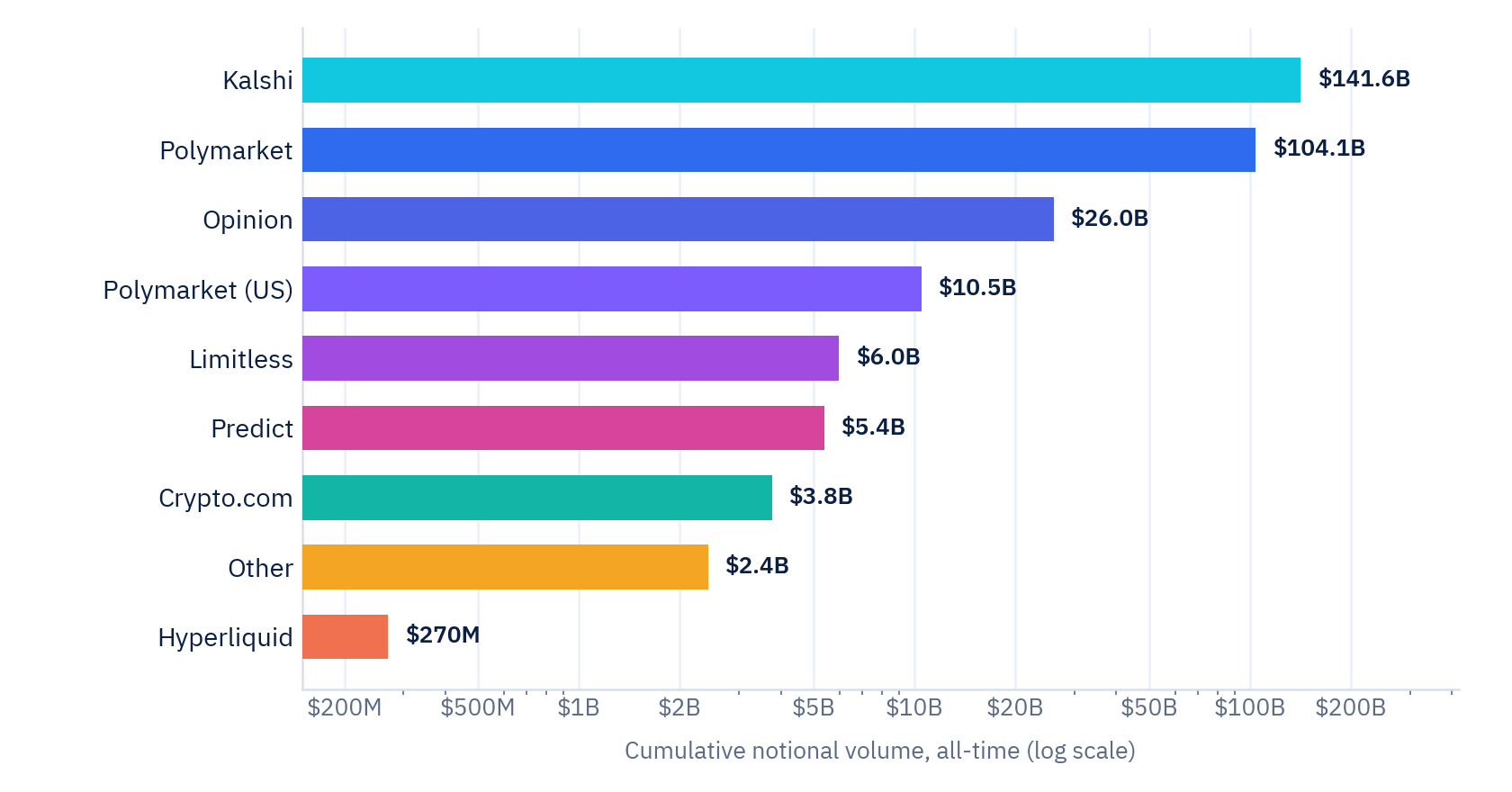

Dune Analytics data puts the sector's all-time, cross-venue notional volume at roughly $300B across nine tracked venues. Kalshi and Polymarket dominate the headlines and, between them, account for about 82% of that total — $141.6B and $104.1B, respectively. But the venue that should be turning heads is Opinion, at $26B: already the third-largest book in the market, ahead of Polymarket's own dedicated US venue at $10.5B, built almost entirely outside the duopoly narrative most coverage repeats uncritically.

The market is bigger and more distributed than the two names everyone defaults to.

Distribution is winning the second half

Which is where the more important thread comes in — the one that actually tells you who wins from here.

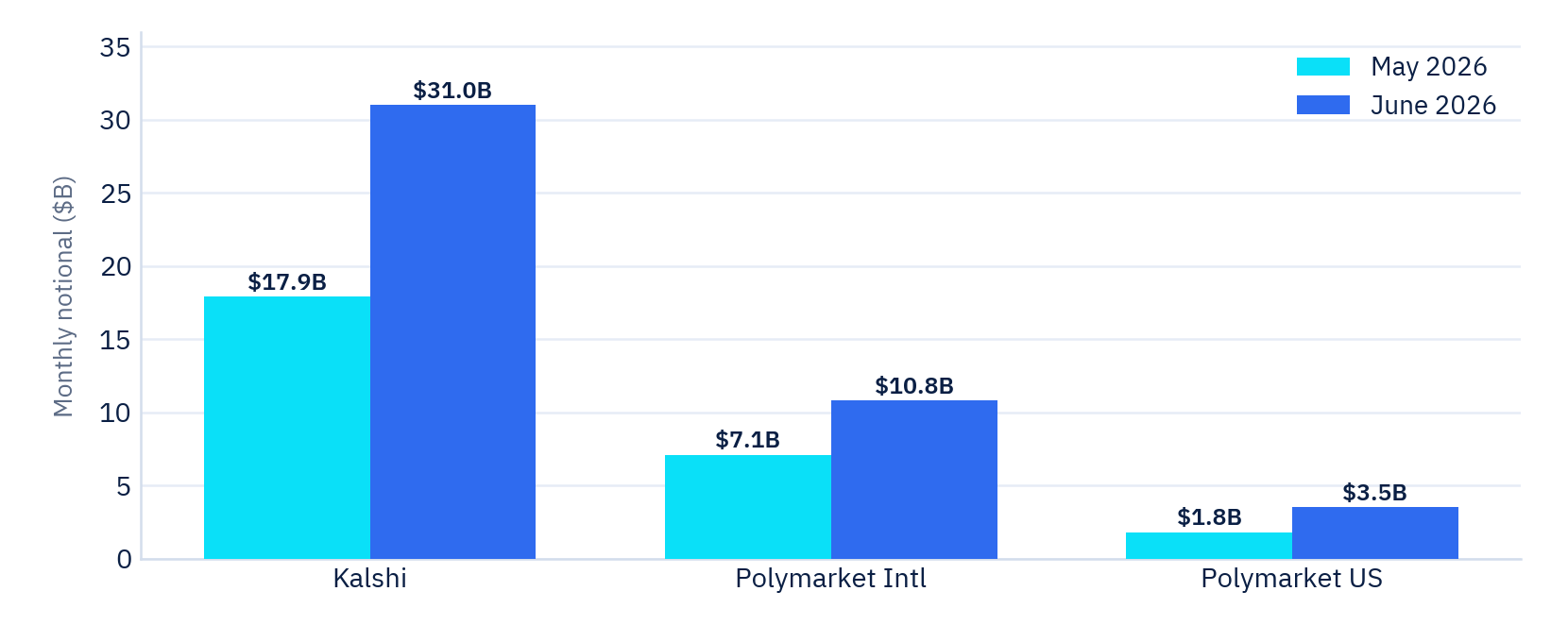

Between May and June 2026, Kalshi's notional volume grew 73% to $31B. Polymarket International grew 53% to $10.8B. Both are real, organic growth numbers for an industry riding a World Cup tailwind. Neither is the most interesting line in the data.

That belongs to Rothera — a joint venture between Susquehanna and Robinhood that didn't exist in May. In its first month of operation, Rothera cleared $2B in volume and now accounts for roughly 7% of all US prediction-market activity. It didn't get there with a better contract, a sharper interface, or a novel resolution mechanism. It got there by plugging directly into Robinhood's existing retail order flow — routing users who were already on the platform, already trading, straight into prediction markets without asking them to go anywhere new.

That's the tell. In a market this young, where contract design is still converging, and most platforms offer functionally similar products, the fastest way to accumulate share isn't a better product — it's a shorter path to users who are already there. Every platform in this space is, whether it says so or not, competing on distribution first and everything else second. Rothera just proved it faster than anyone else has.

The money already agrees

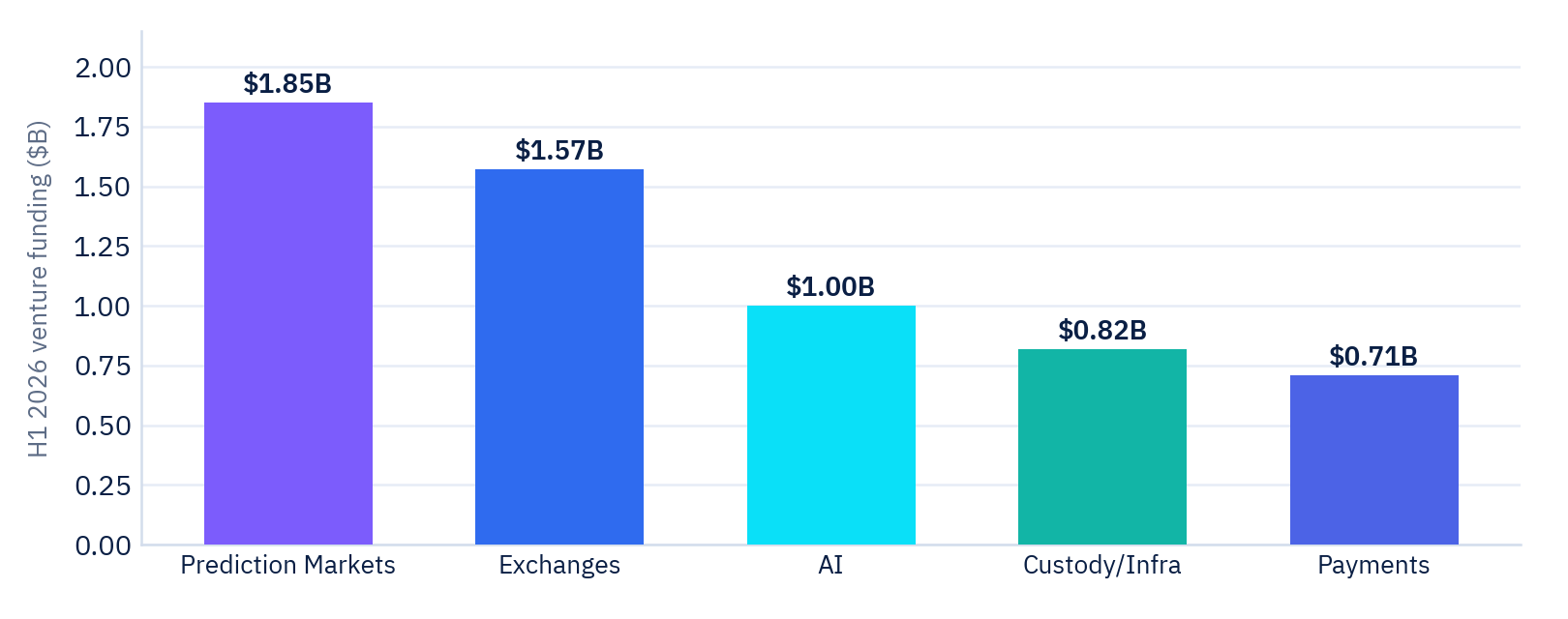

If that thesis needs a second data point, the venture numbers provide one. $1.85B of crypto venture funding went into prediction markets in the first half of 2026 alone — more than went into exchanges, and more than went into AI, the two categories that usually top these tables without contest.

Capital tends to move ahead of consensus, or at least likes to think it does. Here, it's backing the same read the World Cup data just handed us for free: distribution and access are the layer worth owning right now, in a market that has quietly become large enough — and fast-moving enough — to reward whoever gets there first.

What one week actually told us

Put the two threads next to each other, and the picture sharpens. Liquidity in this market concentrates fast around whoever still has genuine conviction and evaporates just as fast around everyone else. Market share concentrates around whoever finds the shortest path to users who are already trading something else. Neither pattern needed a World Cup to exist — the tournament just compressed months of market behavior into one legible week.

This is one week's worth of signal from a market that's still figuring out what it is. The full Prediction Frontier Weekly Data Brief — with the complete venue map, the institutional liquidity read, and what to watch next week — is live now.