What the World Cup Is Teaching Institutions About Prediction Markets

A $64M market went to zero in 90 minutes. Two tournament favourites fell hours apart. What are prediction markets teaching institutions right now?

A $64 million match market repriced to zero in ninety minutes — the most precise live demonstration of how money-weighted probability captures information that analyst models miss.

Two tournament favourites were eliminated within hours of each other by the same binary mechanism — a penalty shootout — offering as clean a real-money illustration of discrete tail-event risk as institutional risk desks are likely to find outside their own models.

The same mechanism that moved Spain from roughly 16% pre-tournament to 10.5% at the knockouts runs on CFTC-regulated venues where Intercontinental Exchange, Susquehanna, Jump Trading, and Jane Street are already building positions.

Institutional capital holds an estimated single-digit percentage of total open interest across the category — the single figure that defines the next phase of prediction-market development.

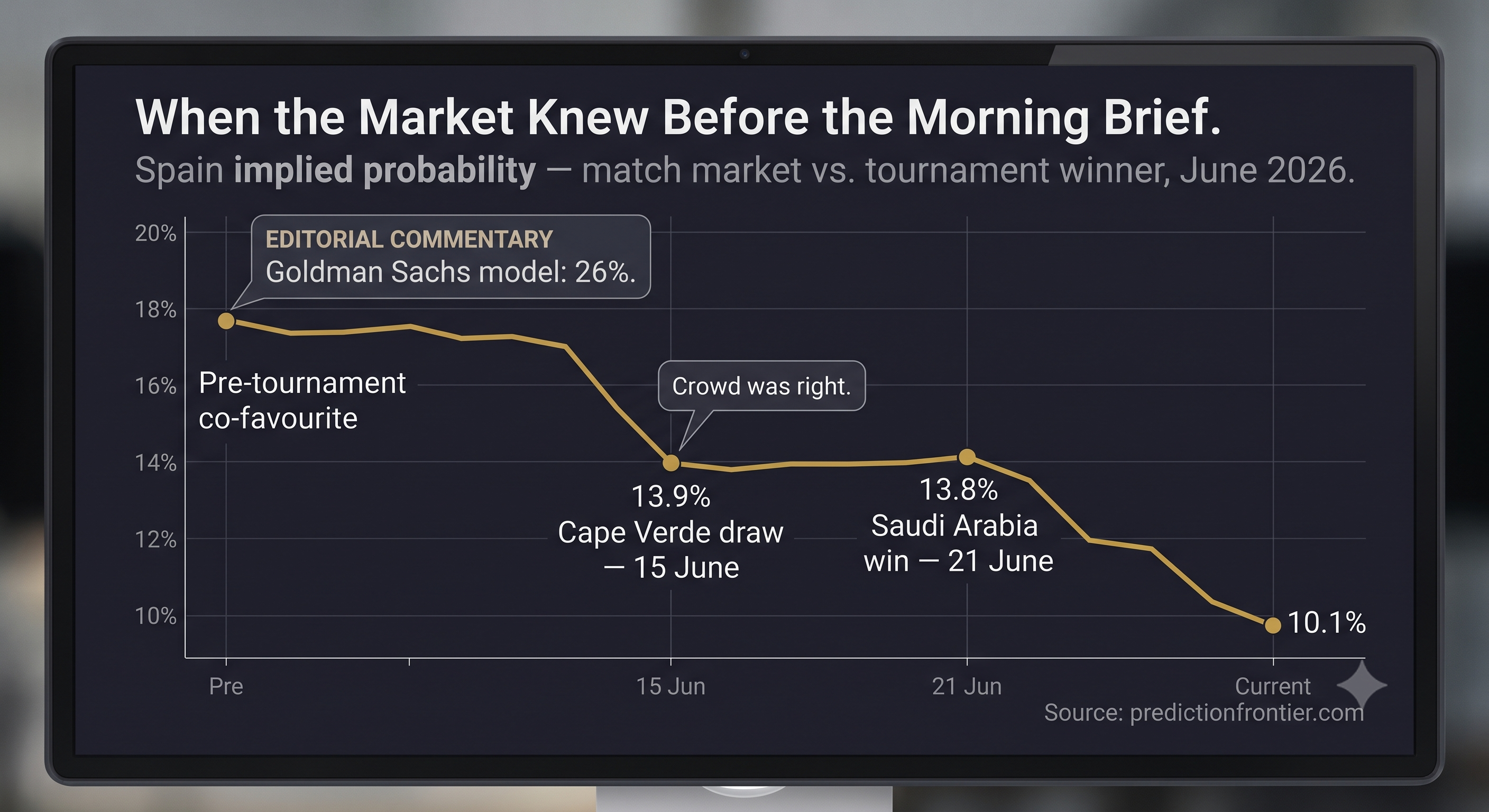

Before the Round of 32 had delivered its first result, this tournament had already produced its defining market moment. On June 15, at Mercedes-Benz Stadium in Atlanta, Spain — reigning European champions, ranked second in the world, thirty matches unbeaten — took the field against Cape Verde. The Atlantic archipelago nation was appearing in a World Cup for the first time in its history. On Polymarket, Spain was priced at 92% to win the match. The draw market stood at 6.6 cents.

Ninety minutes later: 0-0. Spain registered 27 shots. Zero crossed the line.

Sixty-four million dollars of match-market volume repriced to zero at the final whistle. On the tournament winner market — which had already cleared over $2.3 billion at that point — Spain fell from approximately 16% to 13.9% within hours. Goldman Sachs' pre-tournament model, which institutional desks had been running alongside their own forecasts, had placed Spain's title probability at 26 percent. The crowd had been more sceptical all along: the market never followed Goldman above 17%. When ninety minutes of live information arrived, there was no lag, no editorial filter, no morning-after brief. The market moved first, moved fully, and moved in the direction it had been pointing for weeks.

That sequence, compressed into a single evening, is what prediction markets are for. They turn dispersed, money-backed belief into a single number that updates the instant new information lands. And institutions — cautiously through 2024, then with increasing conviction across the first half of 2026 — are beginning to treat that number as infrastructure rather than novelty. Two weeks later, as the tournament moved into its first knockout round, the market delivered a second lesson — sharper and in some ways more useful to an institutional reader, because it wasn't about one team being wrong. It was about what happens when a well-calibrated price meets an event built almost entirely out of variance.

The Information Layer: How Money-Weighted Belief Prices in Real Time

The World Cup winner market on Polymarket has cleared $3.5 billion in cumulative trading volume since it opened in July 2025, making it the deepest single sports prediction market on record. Kalshi surpassed $17.49 billion in notional volume in a single week during the first two weeks of the group stage — a record for the platform — following it up with a record-breaking $30 billion notional volume week last week.

As it stands, France leads as the favourite at approximately 33% on Polymarket and 32% on Kalshi. Argentina, which began the tournament at 8.9%, has climbed to approximately 19% — more than doubling its implied probability without having played a knockout match.

The Argentina repricing carries its own lesson. The move was not driven by results alone, though three group-stage wins and an 8-1 goal aggregate were material inputs. It reflected something compound: thousands of independent positions simultaneously processing Portugal's second-place finish in Group K, which effectively clears Argentina's path to the semi-final, alongside their on-field form. No single analyst produced this estimate. The market assembled it from the bottom up, using money as the weighing mechanism.

The same real-time repricing shows up away from the outright market. Kylian Mbappé's brace in France's 3-0 win over Sweden on June 30 pulled him level with Lionel Messi at six tournament goals each, and the Golden Boot market repriced within the match itself — Mbappé was quoted at 27% on Kalshi as of June 30, among the tightest player-award markets of the tournament.

A smaller, cleaner illustration sat in the United States' own outright price: it opened at 1.6% implied probability, which jumped to 3.9% after a 4-1 win over Paraguay, climbed again to 5.5% after beating Australia 2-0, then eased back to 3.9% following a dead-rubber loss to Turkey with qualification already secured — the market correctly treating a meaningless result as exactly that.

That is what differentiates a prediction market from a model or a poll. A Goldman Sachs forecast updates when Goldman updates it. A poll reflects stated preferences from a sample. A money-weighted probability on a live market updates the instant someone is willing to trade against the prevailing consensus — every trade is an act of disagreement backed by capital. For institutions pricing event risk — a broadcaster purchasing rights inventory, a fund managing exposure to consumer-sentiment indices tied to tournament outcomes, a bank with European equity positions sensitive to French economic confidence — this probability stream is already in use as a real-time signal.

Hedging at Institutional Scale: What Sports Insurance Reveals About Event Contracts

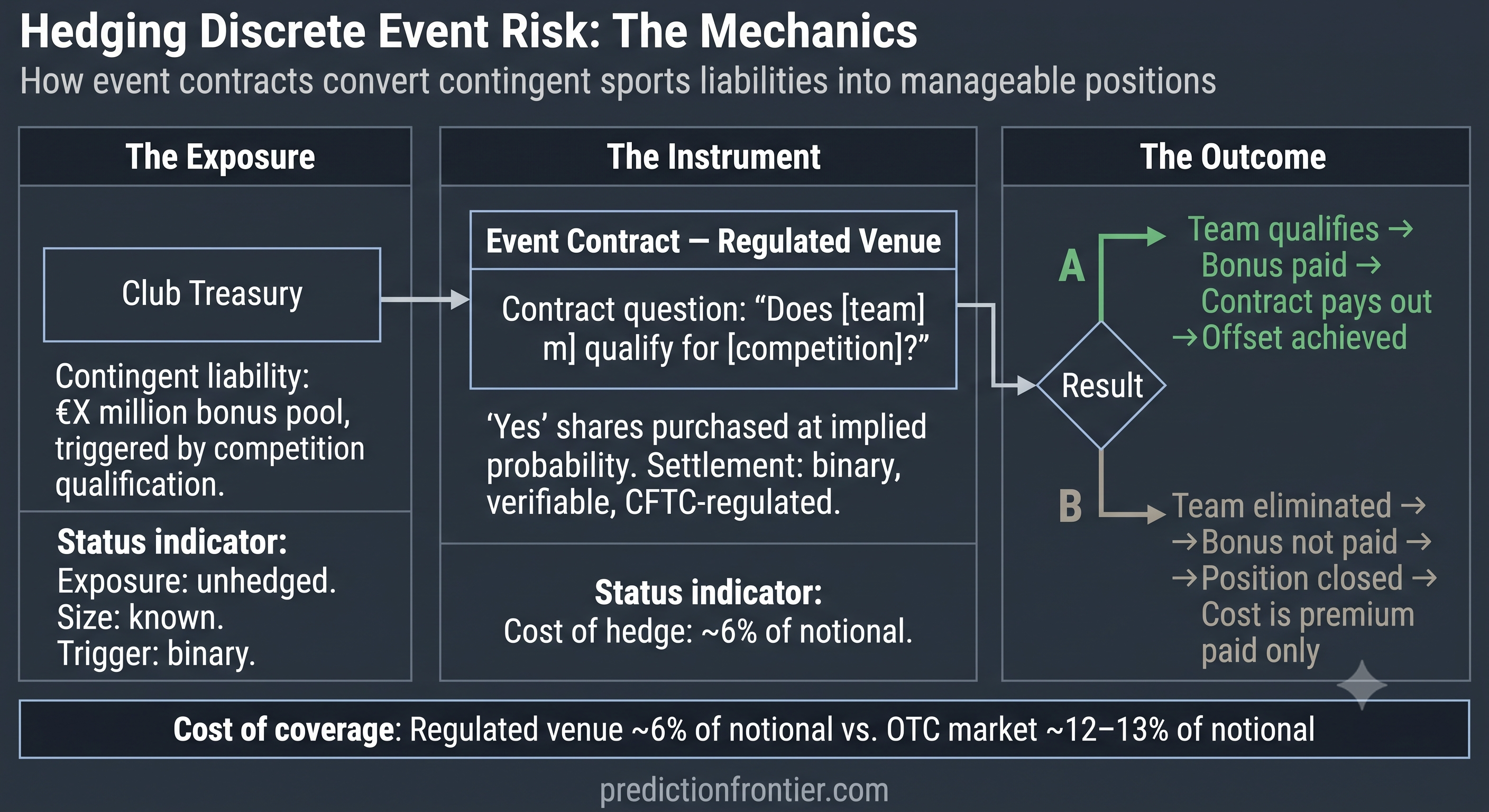

The hedging use case for prediction markets is live and dollar-denominated. Football clubs that advance through knockout competition collect contingent payments tied to results — prize money, broadcaster revenues, performance-linked bonus pools. A club that reaches a major final has materially different finances than one eliminated in the round before. That is a discrete event risk with a known size, a known trigger, and a known settlement date — structurally identical to what event-contract markets are designed to price.

The mechanism has already been priced against traditional reinsurance once, in basketball rather than football: Kalshi's Game Point Capital deal hedged an NBA playoff-berth bonus at 6% versus 12–13% OTC, and a second-round bonus at 2% versus 7–8% OTC — a single transaction, not yet a market average, but the clearest real-money comparison available. The cost differential is material at the scale of a multi-hundred-million-euro bonus pool, and it is the kind of hard, dollar-denominated saving that treasury and finance teams understand without explanation. The sports-insurance application is important for a specific reason: it demonstrates that the demand for event-contract hedging at institutional scale already exists and is already partially served. The constraint is not imagination. It is depth and trust in the regulated layer.

The Microstructure Tell — Reading Mispricing Where Algorithmic Competition Is Still Thin

As of writing, Mexico’s odds of winning the tournament are trading at 5.1% on Kalshi and 3.5% on Polymarket — the same underlying question, priced 1.8 percentage points apart across two regulated, CFTC-overseen venues. The divergence reflects geographic concentration of flow: Kalshi's participant base skews toward the United States, where Mexican-American engagement with the tournament is substantial; Polymarket draws from a more globally distributed pool. Neither platform's price is necessarily wrong in isolation. The structural gap between them is the signature of a market that is young, under-algorithmized, and currently priced by conviction rather than arbitrage.

A second, more explicit illustration sits in a continental roll-up market: a Polymarket contract on which confederation will produce the eventual champion prices Europe at 63% on roughly $8.1M in total volume. While the figure is enough for a retail buyer, an $8.1 M pool is thin enough that a handful of trades from institutional buyers could move it meaningfully. This is precisely the microstructure institutions are evaluating before committing to size.

For institutions oriented toward this microstructure — options-style firms, statistical arbitrageurs, venues building cross-platform products — this is the landscape they have been building toward.

Susquehanna International Group was the first major firm to publicly market-make on a regulated prediction markets venue. Jane Street and Jump Trading are named participants on the regulated side. Trading Technologies has built direct connectivity to bring event contracts to professional terminal infrastructure. Interactive Brokers has launched a prediction-markets platform pooling multiple venues into a single institutional interface. An Acuiti/SGX Global Market Sentiment survey found approximately 9% of institutional derivatives participants already trading prediction markets, with a further third actively weighing entry; proprietary trading firms have moved furthest.

A Coalition Greenwich flash study of US market-structure specialists found that roughly three-quarters expected prediction markets to open new event-speculation channels for institutions within 12 months. Intercontinental Exchange — which has invested in Polymarket — has moved to package crowd-sourced probabilities as an institutional signal feed.

Two Favorites, One Afternoon: Pricing the Discrete Risk of a Penalty Shootout

On June 29, within a few hours of each other, two of the tournament's pre-knockout heavyweights were eliminated — and both by the same mechanism.

Germany had been priced at 6.67% (+1400 on Kalshi) to lift the trophy in the days before the Round of 32 began, placing them in the tournament's second tier of contenders. They drew Paraguay 1-1 through ninety minutes and extra time; Paraguay held their nerve to win 4-3 on penalties. The Netherlands entered its tie against Morocco priced at 5.9% on Kalshi — fifth in the outright field, behind only France, Argentina, Spain, and England. Morocco, by contrast, was priced at just 1.3% to win the tournament outright. And yet in the individual match itself, the market gave the Netherlands only a 59% edge over Morocco — a meaningfully closer call than the 45-point gap in their tournament-winner prices might suggest (Kalshi News, pre-match). The Netherlands led 1-0 through a second-half goal; Morocco equalised in stoppage time and won 3-2 on penalties.

Both contracts resolved to "No" the instant the deciding kick was taken — the same instantaneous, binary settlement mechanic that runs across every market on the board.

The institutional lesson here is a different one from Spain's. Spain's price was wrong about a team's finishing, and the market corrected it. Germany and the Netherlands were not obviously mispriced — a 59% match-winner price for the Netherlands over Morocco was a reasonable reflection of two closely matched sides, and neither team's outright price looked unusual against the rest of the field. What both losses illustrate instead is what a penalty shootout actually is in pricing terms: one of the smallest-sample, highest-variance binary events in professional sport, closer in structure to a single-point election margin or a weather-derivative strike than to a full match, where a larger sample of play lets skill differences show up reliably.

A market can be well-calibrated over ninety minutes and still lose the contract because a shootout compresses a season of quality difference into a handful of essentially coin-weighted kicks. That distinction — between a price being wrong and a price being right but the tail event landing anyway — is exactly the kind of nuance institutions hedging discrete outcomes need to model explicitly rather than average away.

The mechanical consequence was immediate and measurable elsewhere on the board: France's implied probability of winning the tournament moved that same evening — not because France played a match, but because two of the strongest potential obstacles on their side of the bracket had just been removed. Market commentary attributed the move explicitly to this bracket effect. The precise new figure was not captured in this pull and should not be treated as confirmed until a fresh live read is taken; the direction of the move is well-sourced; the magnitude is not.

The Constraint Is Liquidity, Not Appetite — And the Opportunity That Gap Leaves Behind

The category is not mature, and stating this plainly is more credible than pretending otherwise. Institutional capital is estimated by some in the industry to hold a small single-digit share of total open interest — a figure repeated in industry commentary but not traced here to a primary report. The depth constraint is concrete: individual event contracts typically carry between $10 million and $50 million in available liquidity. A single position of $100 million — unremarkable at a mid-sized hedge fund — would move a typical contract by an estimated 20 to 50% on execution. Institutional desks have been explicit: meaningful flow will not route to venues running below approximately $10 million in daily notional volume.

The direction of travel, however, is not ambiguous. Kalshi's annualised volume was reported to have tripled in roughly six months to approximately $178 billion, supported by a reported $1 billion capital raise at a valuation of approximately $22 billion. Industry trackers put 2025 sector volume near $40 billion — a roughly fourfold increase on the prior year — with analyst projections, including from Bernstein, pointing toward the order of $1 trillion by 2030. The speed of the market's movement toward institutional infrastructure is visible: the named participants, the regulatory clarity, the cross-platform connectivity, the first customised block trades. What is not yet built is the per-contract depth that allows serious position sizes to execute without material market impact, or the settled commercial and regulatory language around how platforms and the events they price relate to one another. Appetite is confirmed. Liquidity and institutional-grade clarity are the remaining work.

▶ The World Cup is a live prediction markets classroom. Watch the explainer series on YouTube — search Prediction Frontier — for weekly breakdowns of market mechanics behind the knockout results.

Not financial or investment advice. Prediction markets involve real-money event contracts and carry the same behavioural and financial risks as any speculative activity. All figures are drawn from public market data and third-party reporting; verify all live data before relying on it for any purpose. Figures labelled as estimates, approximations, or reported should be treated as directional, not audited.

Follow @PredictionFrontier for ongoing World Cup market analysis and institutional prediction markets intelligence.